Since our initial report on Pharmacyclics (PCYC) on February 11, shares of the oncology company have returned almost 52%. Pharmacyclics’ relative underperformance to the NASDAQ Biotechnology Index in that timeframe is a result of a precipitous decline from an all-time high of over $143 in October to a under $100 by December (shares currently trade at under $108). However, the decline has not been caused by materially adverse news. Pharmacyclics has not released negative clinical data, and in fact the company secured FDA approval for Imbruvica in November, paving the way for a meaningful ramp in revenue. Technical selling and a turnover in its shareholder base have contributed to Pharmacyclics’ decline as the company shifts from a development-stage biotechnology company into a commercial-stage company.

In our view, long-term investors should utilize Pharmacyclics’ recent decline to add to or initiate positions ahead of new Phase III data for Imbruvica due in Q1 2014. With a pristine balance sheet and the backing of Johnson & Johnson (JNJ), Pharmacyclics is positioned to begin channeling Imbruvica’s clinical profile into robust revenues and profits.

The Shift to the Commercial Stage Begins

Pharmacyclics announced on November 13 that the FDA has granted approval to ibrutinib for the treatment of mantle cell lymphoma (MCL) for patients that have had at least one prior therapy; the drug will be marketed under the trade name Imbruvica. The approval of Imbruvica entitles Pharmacyclics to yet another milestone payment under its partnership with J&J, this time to the tune of $60 million. This comes on top of $75 million in milestone payments received in August for the acceptance of the company’s NDA’s for ibrutinib in MCL and CLL (the CLL NDA is still under review). The approval of Imbruvica will pad Pharmacyclics’ already robust cash balance; as of the end of Q3 2013, the company held $560.1 million in net cash & investments, or $7.59 in net cash per share. Pharmacyclics’ partnership with J&J has been highly lucrative, and more importantly, the staggered nature of the deal has served to limit dilution for Pharmacyclics’ investors. We remind investors of the following key points of the collaboration agreement between the two companies:

- $825 million in aggregate milestone payments: in total, Pharmacyclics is entitled to $825 million in milestone payments tied to various clinical, regulatory, and commercial milestones. To date, Pharmacyclics has booked a total of $385 million in payments ($275 million as of the end of Q3 2013, $50 million for the filing of an Ibrutinib MAA in Europe, and $60 million for the FDA approval in MCL)

- Profit & cost sharing: Pharmacyclics will recognize Imbruvica sales in the United States, with international sales recognized by J&J. While profits will be split equally between the companies, Pharmacyclics is required to pay only 40% of the development costs of Ibrutinib, and Pharmacyclics’ Imbruvica development and commercialization costs are capped at an annual rate of $50 million until the third profitable quarter for Imbruvica.

With costs capped by its agreement with J&J, and over $400 million in milestone payments remaining, Pharmacyclics’ cash burn will be limited throughout Imbruvica’s initial commercialization. And with over $560 million in net cash, it is highly unlikely that Pharmacyclics will have a need to raise new capital, given that it is expected to be profitable in both 2013 and 2014, albeit primarily through milestone payments as Imbruvica sales ramp higher. Pharmacyclics is moving towards sustainable profitability, the “easy” money in the stock has been made, and although we see meaningful value remaining in Pharmacyclics from a long-term perspective, gains will not come overnight – Investors must contend with a new slate of concerns.

Food for Bears: Derailing Imbruvica’s Potential

For Pharmacyclics investors, the years spent developing Imbruvica were both profitable and relatively simple. In essence, as long as the drug kept generating promising clinical data (with a corresponding increase in peak sales estimates from Wall Street), PRCYC had an easy climb. But now the picture is nuanced. The determination over whether or not Imbruvica is posting “good” results is no longer black or white, and for many investors this is a new phenomenon. For over 18 years, Pharmacyclics’ investors have analyzed it as a clinical-stage company, and as it transitions to the commercial stage, turnover in the company’s shareholder base is inevitable. This turnover has likely played a role in the company’s recent selloff, as have several points of concern over potential competition for Imbruvica.

At its core, investing in biotechnology is all about the future. Billions are made and lost based on assessments of a company’s future prospects, and investors in the sector are always willing to turn their attention to the next potential blockbuster. Now that Imbruvica has secured FDA approval, investors are only too willing to turn their attention elsewhere in an attempt to find new drugs that can derail Pharmacyclics. Chief among this slate of new competitors is Ono Pharmaceuticals’ ONO-4059, a BTK inhibitor now in Phase I trials (NCT01659255). ONO-4059 is being tested as a monotherapy in relapsed/refractory NHL and CLL; the FDA is currently reviewing Imbruvica for use in CLL (there are currently no clinical trials testing Imbruvica in NHL). Although the Phase I study ONO-4059 will not be complete until April 2016 at the earliest, there is cause for concern today. At ASH 2013, Ono Pharmaceuticals in collaboration with Roche (RHHBY) presented pre-clinical data highlighting the synergistic effects of a combination treatment of ONO-4059 and Obinutuzumab (GA101 or RG7159) versus ONO-4059 in combination with Rituxan. Given that Roche provided funding for the trial, investors are following events to their logical conclusion – that Roche will license ONO-4059 and add it to its diverse slate of oncology therapies. The results of the pre-clinical trial showed that a combination treatment of ONO-4059 and GA101 resulted in tumor growth inhibition of 90%, versus 86% for ONO-4059 in combination with Rituxan. In addition, the ONO-4059/GA101 combination led to tumor remission in 30% of animals (3/10), versus just 10% (1/10) for the ONO-4059/Rituxan combination. We note that as a monotherapy, ONO-4059 did not result in tumor remission, and posted a tumor growth inhibition rate of 63%.

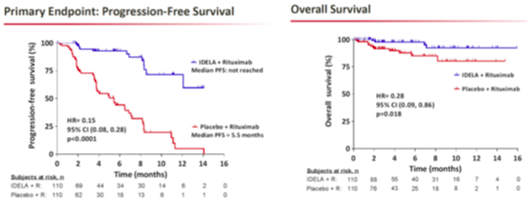

In addition to news from Ono and Roche, Gilead Sciences’ (GILD) idelalisib is moving ahead; the drug is already under FDA review for the treatment of indolent non-Hodgkin’s lymphoma (iNHL) and has secured breakthrough therapy status in CLL in the United States. Gilead presented Phase III data for idelalisib in combination with Rituxan (versus Rituxan in combination with placebo) for the treatment of CLL at ASH, with impressive results.

The Phase III trial showed statistically significant efficacy; a pre-specified interim analysis showed that progression-free survival has not yet been reached; and with a hazard ratio of 0.15 (p<0.0001) the results were significant. The improvement in overall survival was also statistically significant, with a hazard ratio of 0.29 (p=0.018). Safety was generally acceptable, with the most common adverse events being pyrexia (29% rate in the idelalisib/Rituxan arm, 16% rate in the control arm), fatigue (24% vs. 27%), nausea (24% vs. 22%), and infusion-related reactions (16% vs. 28%). Serious adverse events included pneumonia (6.4% vs. 8.4%), and pyrexia, which occurred in 6.4% of patients in the idelalisib/Rituxan arm. And while elevations in liver enzymes were noted, they appear to be manageable, and a data monitoring committee recommended that the trial be halted due to its strong efficacy and safety profile.

As Credit Suisse has noted, the potential implications for Pharmacyclics and Imbruvica go beyond positive data for Rituxan/GA101 combination therapies. The firm notes that oncologists and hematologists have, as a result of Roche’s dominance in the field, become trained to prescribe Rituxan, and the market is prepared to deliver intravenous therapies such as Rituxan and, assuming approval, GA101. The market may resist switching to Imbruvica’s all oral dosing due to the impact this would have on the profitable intravenous delivery market, especially if there is compelling clinical evidence to support Rituxan/GA101-based combination treatments.

As it comes into being as a commercial-stage company, Pharmacyclics will not be competing with a collection of development-stage oncology companies. Rather, it will be competing against some of the largest biotechnology and pharmaceutical companies in the world, including Roche, Gilead, as well as Celgene (CELG) (via CC-292). And while Pharmacyclics does have the backing of Johnson & Johnson (JNJ), its competitors are all companies for whom the financials are irrelevant. Furthermore, Imbruvica’s safety profile, while generally clean, has come under scrutiny, particularly in CLL. Existing clinical data for Imbruvica in CLL shows that patients have seen progression into Richter’s transformation, a rare (5% incidence rate in CLL) and often fatal complication of CLL. While the incidence rate of Richter’s transformation is low, there is concern that the FDA will include a black box warning for Imbruvica in CLL. Credit Suisse has noted that an outcome is unlikely; the above-average incidence rate of Richter’s transformation in Imbruvica’s CLL trials is a byproduct of its leading progression-free survival data in CLL (more on this later); given that CLL patients taking Imbruvica are living longer, it is logical to conclude that there will be higher rates of Richter’s given that these patients are living long enough to actually see complication.

As competitors move their compounds through development, Pharmacyclics’ investors have become concerned, given the solid results that they have posted, as well as the fact that the companies developing them have essentially unlimited financial resources, thereby negating the advantage of having Johnson & Johnson as a partner. While these are valid concerns, we believe that in the long run they will not derail Pharmacyclics. The company is well positioned, and as key clinical data are set to be released in Q1 2014, investors should retain exposure to the company.

Food for Bulls: Leveraging First to Market Status

With approval in MCL, Imbruvica is now the first to market amongst the next generation of hematology treatments (a group that includes IPI-145, idelalisib, GA101, ONO-4059, etc.), and the importance of this distinction should not be overlooked. Although Imbruvica is currently approved only in MCL, there is already anecdotal evidence, according to Wall Street analysts, of off-label prescribing, and more importantly, off-label reimbursement in CLL and WM (Waldenstrom’s macroglobulinemia, for which Imbruvica is now in Phase II trials). While this trend may not be widespread throughout the oncology community, it is nevertheless positivedemonstrating that awareness of Imbruvica is high. As its label widens, there will already be an embedded base of support for the drug. Imbruvica’s portfolio of clinical data is already expanding. The drug is included in the National Cancer Institute’s long-term (primary completion date is March 2018) Phase III CLL trial (NCT01886872), which features three arms: a control arm of Rituxan, Imbruvica as a monotherapy, and Imbruvica in combination with Rituxan (the primary endpoint is progression-free survival, with several secondary endpoints, including overall survival, duration of response, toxicity, and quality of life). In addition, there are further intergroup studies being conducted, testing FCR vs. Imbruvica and Rituxan, and BR vs. Imbruvica vs. Imbruvica vs. Rituxan. These intergroup trials are key in altering treatment regimens and setting the bar for clinical efficacy, and given its first to market position, Imbruvica’s inclusion in these studies is a key long-term advantage for the drug. And with new Phase III CLL data set to be released, Pharmacyclics will have the potential to further solidify Imbruvica’s proposition as the CLL standard of care.

Phase II data for Imbruvica in CLL showed a 30-month progression-free survival rate of 69.7% in relapsed/refractory patients, and 95.8% in treatment-naïve patients, a result that Credit Suisse notes has yet to be matched by any therapy, either as a monotherapy or in combination. We note that while median PFS has yet to be reached in the Phase III idelalisib/Rituxan study, the survival rate at 14 months is around 60%, far below Imbruvica’s results. And with interim Phase III CLL data approaching, Pharmacyclics investors will soon have a chance to see new CLL data.

Even as Imbruvica is under review by the FDA for approval in CLL (thanks to its breakthrough therapy designation), the company is conducting its Phase III CLL program. The program is split into several trials, including RESONATE (NCT01578707) and RESONATE-2 (NCT01722487). With 391 relapsed/refractory patients, RESONATE tests Imbruvica (dosed orally once per day) against GlaxoSmithKline’s (GSK) Arzerra (ofatumumab), with progression free survival serving as the primary endpoint; secondary endpoints include overall survival and improvement of disease-related symptoms. Although RESONTA has a primary completion date of July 2015, an interim read out will occur in Q1 2014, allowing investors to compare Phase III Imbruvica results to Phase III idelalisib and Rituxan results. RESONATE-2, with a primary completion date of June 2015, has enrolled 272 treatment-naïve patients into one of two arms: either Clorambucil or Imbruvica, with progression free survival serving once again as the primary endpoint. An additional study, RESONATE-17 (NCT01744691) is testing Imbruvica in relapsed/refractory CLL patients with the 17p deletion. Assuming that the interim RESONATE data is positive, Imbruvica has a chance to maintain its position as the leader in progression-free survival, and given its status as a monotherapy, the drug has a chance of emerging as a new standard of care in CLL

We note that many of the trials involving potential competitors to Imbruvica (ONO-4059 and idelalisib) were conducted in a conventional “add-on” approach, with Gilead and Ono Pharmaceuticals seeking to determine whether or not their drugs can convey benefits in addition to an existing therapy. But, given Imbruvica’s status as a monotherapy, future studies will likely seek to determine whether other therapies convey benefits in addition to Imbruvica. In this setting, it is Imbruvica, not Rituxan that forms the core of a CLL treatment regimen. Already Pharmacyclics and Johnson & Johnson are testing a combination. The HELIOS trial (NCT01611090) is a Phase III trial (primary completion date is August 2015) with 580 relapsed/refractory CLL patients placed into one of two arms: Imbruvica and Rituxan or Rituxan and placebo, with progression-free survival serving as the primary endpoint (secondary endpoints include overall survival and overall response rate). With solid data in CLL, Pharmacyclics is poised to generate meaningful sales if and when Imbruvica secures approval. While peak sales estimates for Imbruvica range from $6-$9 billion, CLL forms the core of the drug’s potential; Goldman Sachs’ $7.5 billion peak sales estimates includes $5 billion in sales from CLL alone, with the remaining $2.5 billion spread throughout Imbruvica’s other indications (MCL, multiple myeloma, Waldenstrom’s macroglobulinemia, follicular lymphoma, and diffuse large B-cell lymphoma).

Conclusions

Pharmacyclics’ recent selloff has created an opening for long-term investors to add to or initiate positions in the company ahead of the interim RESONATE analysis and what is shaping up to be a key year for Pharmacyclics. With a strong balance sheet and the backing of Johnson & Johnson, Pharmacyclics is well positioned as it enters the next stage of its corporate life cycle, and we believe that in 2014 investors stand to profit from Imbruvica’s emerging blockbuster potential.

In connection with PCYC, PropThink has taken a long position.