The early innings of the obesity landscape is starting to take shape, and it seems to be forming similar patterns to that of checkpoint inhibitors from a decade ago. There are backbone drugs, the ones with first mover advantage, fast followers who are hopeful and combinations – many of which will disappoint. Let’s compare.

GLP-1 Shaping Up to Be the “PD-1” of Obesity

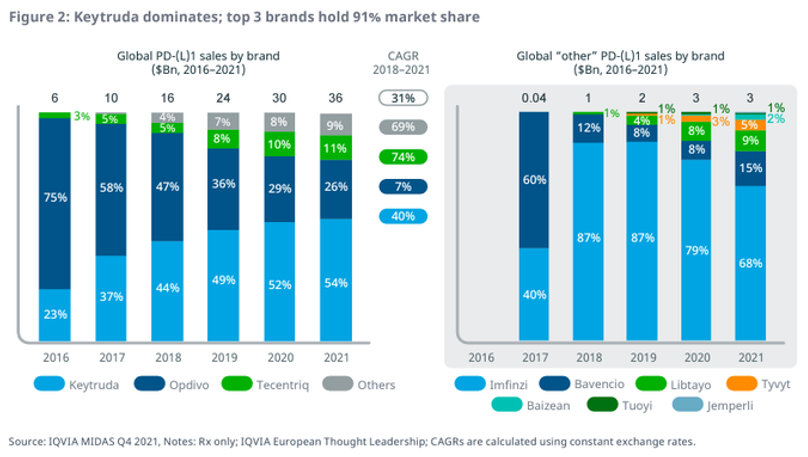

Immunotherapies, particularly checkpoint inhibitors PD-1s & PD-L1s, have been transformational for oncology treatments. Merck’s pembrolizumab (“Keytuda”) was first approved in 2014 and has become a $30B/year behemoth and the best-selling drug. Bristol’s nivolumab (“Opdivo”) is a distant second with about $10B/year. With 10 years of data now, we’ve seen how this market has played out. PD-1s are the backbone immunotherapies for cancer.

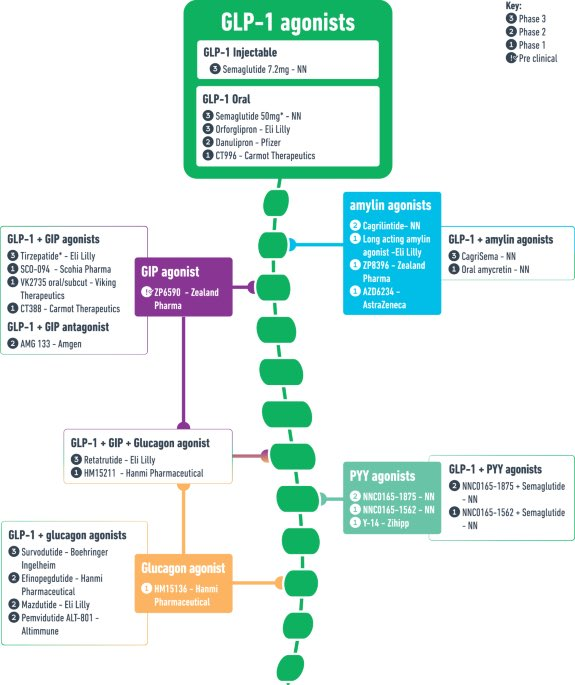

GLP-1 is the backbone of obesity. It will be difficult for other mechanisms to provide the same monotherapy efficacy as GLP-1. Other approaches (GIP/CB1/amylin – more on these later and in follow on notes), might try to go head-to-head with GLP-1, but are likely to disappoint as, and will ultimately settle for being combinations or acting as niche treatments for “GLP-1 non-responders or population sub-segments”. This isn’t a bad thing as type 2 diabetes/obesity are such large addressable markets, that even niche segments are billion dollar opportunities.

Eli Lilly & Novo Nordisk Are Leaders & Will Likely Stay There

If Merck & Bristol’s success with PD-1 showed anything, it is that the first mover advantage is difficult to dethrone. There are now 9 approved PD(L)-1s, yet Keytruda dominates with more than 50% market share. According to IQVIA, the top 3 PD(L)-1s have greater than >90% market share.

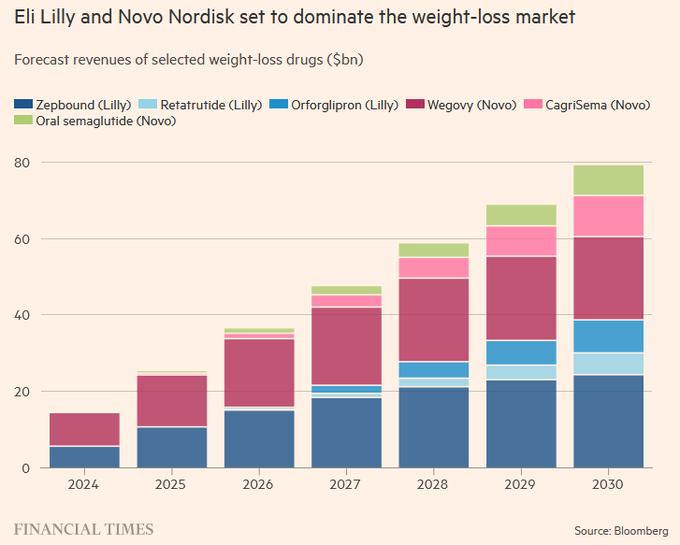

It’s expected that the same is going to happen in obesity. Lilly’s & Novo’s GLP-1 franchises are projected to generate $10B+ and $20B+, respectively in 2024. The same is being forecasted out into 2030, whereby Lilly & Novo are going to generate about $80B of the ~$100B market.

This leaves late-comers Roche, AstraZeneca, Novartis, Pfizer, Amgen and smaller player Viking with a fraction of the market, approximately $20B. Still more than enough to go around, but these late comers will need to differentiate & innovate to get a larger piece. So far, Viking’s VK2735 & Amgen’s AMG-133 have shown a differentiated enough profile in Phase 2 to challenge the top two players. Both will need to replicate these results in larger trials, which is no small task.

Obesity Combinations Will Be a Rising Trend

With GLP-1 being established as the backbone to obesity, companies will now focus on offering incremental benefits. The same way that PD-1 has been combined with a plethora of approaches over the last decade. IL-2, TIM3, TIGIT, ICOS, CD47 to name a few. These came up short of expectations, but there were also winners -Bristol Myers Squibb’s LAG3 (Opdualag) + CTL4 (Yerovy), both of which are expected to be multi-billion dollar drugs.

A similar pattern is playing out in obesity as companies are trying novel approaches to (eventually) combine with GLP-1.

- Myostatin to preserve the muscle loss

Lilly acquired private company Versanis for $1.9B and Regeneron is repurposing old muscular dystrophy antibodies. We covered the myostatin players here, including Biohaven (BHVN), Scholar Rock (SRRK) and Keros (KROS).

- APJ for improved body composition

Similar to the myostatin thesis, apelin receptor APJ agonists are believed to improve body composition in combination with GLP-1 drugs. Apellin is a peptide that is released in response to exercise, thus leading to the approach as way of preserving muscle mass while losing weight. Bioage (BIOA) recently completed a $238M IPO for their azelaprag in Phase 2 studies in combination with GLP-1 drugs. Structure (GPCR) also has an APJ agonist in Phase 2 called ANPA-0073.

- CB1 in non-incretin approach

Last month Novo Nordisk announced results from a phase 2a with monlunabant, a small molecule oral cannabinoid receptor 1 (CB1) inverse agonist. Monlunabant, formerly INV-202, was part of the $1B acquisition of Inversago in August 2023. Although CB1 monotherapy weight loss data was not equivalent to GLP-1, it did show a 5.8% weight loss placebo reduction at 16 weeks. To compare, GLP-1 are routinely demonstrating 7% placebo adjusted reduction at 12 weeks. The bigger concern was raised from the mild to moderate neuropsychiatric side effects, primarily anxiety, irritability, and sleep disturbances. Even with this so-so data, Novo is moving forward with a larger phase 2b trial, initiating in 2025.

Time will tell what happens with CB1, but a potential path going forward could be combining it with GLP-1s so that patients take a smaller dose of the GLP-1—which could lead to fewer gastrointestinal side effects and a greater chance of adherence to the medication regimen.

Corbus (CRBP) and Skye (SKYE) are in clinic with their own CB1 blockers.

- Mitochondria uncouplers to increase energy consumption

Rivus (private) reported data for their HU6 mitochondrial uncoupler in heart failure patients. At 3 months, HU6 reported 2.7% placebo-adjusted fat mass loss. Although not as much weight loss as GLP-1s, this approach burned all fat and no muscle, which is promising given the combination potential with appetite suppressing drugs like GLP-1. Rivus is expected to complete a $250M IPO as soon as this year, according to Bloomberg.

- Amylin expected to be the next big target

Amylin analogs are a different modality (non-incretin) as it works by increasing satiety and increasing leptin sensitivity, which is a distinct mechanism compared to GLP-1. Novo and Lilly are leaders in this amylin space with Novo’s CagriSema in Phase 3 and Lilly’s long acting amylin. The rest of the amylin analogs are in early stage, with two Danish companies Zealand (ZEAL in Copenhagen market) and Gubra (GUBRA in Copenhagen) being the two smaller names. We’re going to do a deeper dive into amylin in a follow on report, as early data has shown promising enough results to be comparable to GLP-1.

The obesity market is showing some similar characteristics to how checkpoint inhibitors played out. Merck was the winner from the PD1, due to their blockbuster Keytruda. Bristol (BMY) was a distant second. As it stands, Eli Lilly (LLY) and Novo Nordisk (NVO) are the two obesity leaders with their existing marketed drugs, and broad metabolic pipelines targeting multiple approaches. Over the last years, money was made trading, rather than holding, the other non-PD1 targets as the majority ended up flopping. We think a similar trading strategy will prove to be most profitable for the smaller obesity names.

PropThink contributors do not hold any positions in the companies mentioned.