In December, Bellus Health (BLUSF:OTC) (BLU:TSX) will report Phase 1 data for their chronic cough candidate BLU-5937. Bellus’ candidate is a P2X3 inhibitor, a class of drugs that have shown the most promise as a chronic cough treatment and has demonstrated early signs of success. We think there is a strong likelihood this data will be positive, positioning Bellus as the best-in-class candidate for a multi-billion dollar indication and fairly valuing the company at $1.25/ share, or roughly 65% higher than current market price.

Refractory Chronic Cough is a $2 Billion+ Market with No Viable Treatments

There are approximately 2.6 million people in the US with cough lasting longer than 1 year. Current treatment options for these refractory cough patients are inadequate. OTC cough products have little scientific data supporting their effect, while prescribed medications, such as codeine, cause temporary relief, but are connected with adverse effects like drowsiness and risk of abuse.

The market opportunity in chronic cough was validated in the summer of 2016 when Merck acquired private company Afferent Pharma for $500 million upfront and up to an additional $750 million in milestones. At the time of the acquisition, Afferent was in Phase 2 development for a candidate that inhibits the P2X3 receptor, which triggers the cough reflex. Merck’s bet, which could amount to $1.25 billion in total, supported the chronic cough market as a multi-billion dollar indication with an unmet need.

P2X3 Drug Class Has Shown Most Promise in Reducing Cough

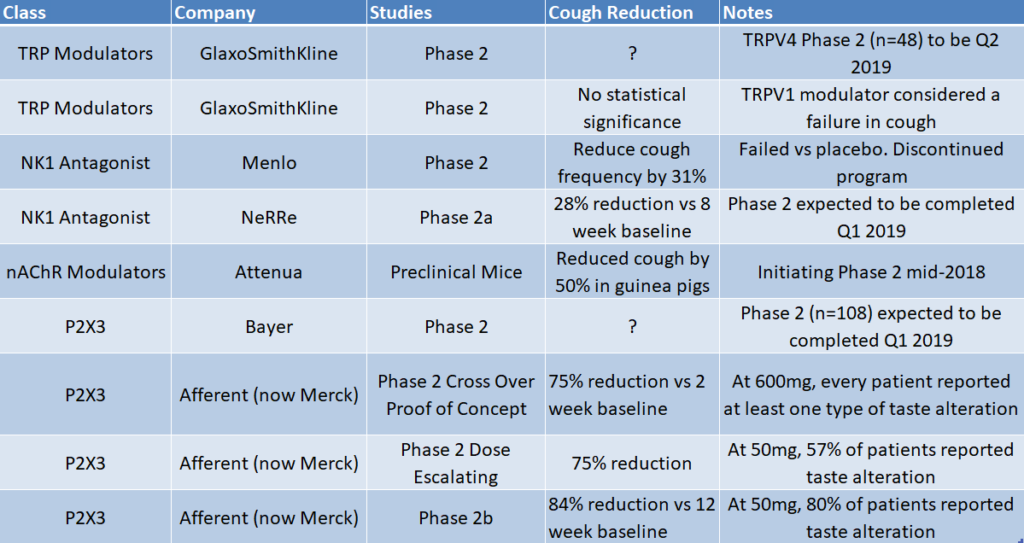

Cough is a protective reflex to clear the lungs/airways of harmful particles, so it has become common opinion that chronic cough is a neuropathic disorder. Therapies in development are targeting different sensory receptors that are believed to initiate the cough reflex. The landscape is dominated by 4 main drug classes (Figure 1, below):

- P2X3 Inhibitors

P2X3 is a sensory receptor found in the nervous system. Excessive activation of P2X3 receptors are associated with hyper-sensitize sensory neurons in the airways and lungs, which trigger the urge to cough. P2X3 inhibitors work by regulating P2X3 expression and thus reducing coughing urges.

Compared to the other drug classes, P2X3 candidates have reported the most data and the highest efficacy in reducing chronic cough. In a Phase 2b (n=253), MK-7264 reduced cough by 86%. Merck’s P2X3 candidate is currently in Phase 3 while Bayer is expected to complete their Phase 2 study for a selective P2X3 candidate in Q1 2019.

- TRP Modulators

Studies have shown that the cough reflex is induced by activation of airway sensory nerves and TRPV ion channels. Blocking these TRPV channels may lead to improved cough symptoms. GlaxoSmithKline (GSK) is testing this thesis in Phase 2 proof of concept studies of their candidate GSK-2798745, a TRPV4 channel blocker. The study is expected to be completed in April 2019 and will report number of coughs during day-time hours. Keep in mind, GSK’s other TRP candidate did not show an improvement in cough frequency vs placebo.

- NK-1 Antagonists

Substance P (SP) and the neurokinin-1 receptor (NK-1) have been shown to trigger several reflexes. Blocking SP at the NK-1 receptor may hinder the signaling process and improve urges like cough, itch-scratch reflex and vomiting. Private biotech NeRRe Therapeutics and Menlo (MNLO) are developing NK-1 antagonists with hopes of stopping these urges.

In a proof of concept Phase 2 study (n=13), NeRRe’s Orvepitant demonstrated a 28% reduction in cough after 8 weeks. A larger Phase 2 study (n=244) is expected to read out Q1 2019.

Menlo’s (MNLO) serlopitant failed Phase 2 (n=185) in chronic cough with 31% reduction. Menlo discontinued development after this failure. With Menlo's failure, NK-1 candidates are indicating they are not as effective as P2X3 in reducing cough.

- nAChR Modulators

Nicotinic acetylcholine receptors (nAChRs) modulate the flow of signals throughout the brain and nervous system, both of which are important in breathing rhythm and cough. The nAChR has also been co-expressed with TRPV channels that induce cough. In theory, blocking these receptors can deter cough reflexes.

Private company Attenua reduced cough in preclinical studies by about 50% with their nAChR candidate AT-101. The company will be initiating Phase 2 mid-2018.

Figure 1: P2X3 drug class is the most clinically advanced in chronic cough and has reported the best data to date

Key Takeaways:

- P2X3 drug class has shown the most promise and is the most clinically validated drug class with numerous human studies.

- Past data that has been released for TRP modulators and NK-1 antagonists have not shown the same promise as P2X3. This does not instill confidence for upcoming TRP & NK-1 data readouts.

- Merck’s P2X3 drug is the most advanced candidate (currently in Phase 3) and has shown 86% reduction in cough after 12 weeks. To compare, NeRRe’s NK-1 candidate reported 31% reduction in cough after 12 weeks.

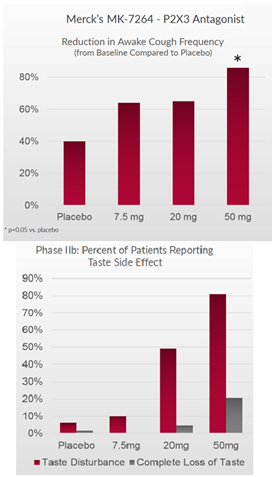

The Current Best in Class P2X3 Drug Was Acquired for $500 Million Upfront; But It Was Burdened With Taste Side Effects

Merck made a big splash in chronic cough when it acquired Afferent for $500 million upfront based on early Phase 2 studies. After the acquisition, Merck released data from a larger Phase 2b study (n=253), where MK-7264 showed an 86% reduction in cough frequency from baseline at 12 weeks. This was statistically significant vs placebo (p=0.001) at Merck’s highest tested 50mg dose (twice daily). It’s important to note that the two other tested doses, 7.5mg and 20mg did not show statistical significant vs placebo. This could be due to the placebo arm showing 39% reduction in cough, which was higher than anticipated.

Although MK-7264 showed great efficacy, it was burdened with a taste disturbance that was reported in 80% of patients. 20% of patients reported a complete loss of taste. Despite this, Merck has decided to proceed advance the program with two large Phase 3 studies (720 and 1290 patients, respectively).

Figure 2: MK-7264 has shown a positive correlation between higher dose, cough reduction and taste disturbance

It is widely believed that the taste side effect from Merck’s drug is because the drug inhibits the P2X3 receptor that reduces cough and the P2X2/3, a cousin receptor found in taste buds. The drug’s weak selectivity could explain why the higher the dose, the more effective it is at reducing cough, but also causing greater taste loss.

This presents an opportunity: develop a drug that inhibits P2X3 (cough receptor) but does not inhibit P2X2/3 (taste receptor).

Bellus is Developing a Selective P2X3 Candidate That We Expect to Show Equivalent Cough Reduction & Minimal Effect on Taste

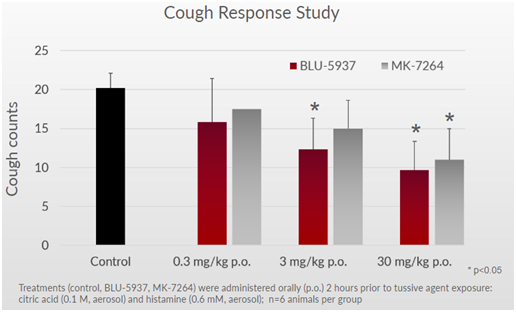

Bellus’ candidate, BLU-5937, has shown to be a selective P2X3 inhibitor that targets the P2X3 receptor to reduce cough and avoids the P2X2/3 receptor to maintain taste function. This hypothesis has been demonstrated in preclinical studies, where mice taking BLU-5937 or MK-7264 showed similar cough counts at various doses (Figure 3 below).

Figure 3: BLU-5937 reduces histamine induced cough at similar rate to MK-7264

It’s important to note that in human cell assay studies, BLU-5937 was 10x more potent than MK-7264 for the P2X3 receptor, implying that BLU-5937 can show greater efficacy in reducing cough. In animal assays, the potency between both candidates was similar, which can explain why the efficacy in preclinical data above is similar.

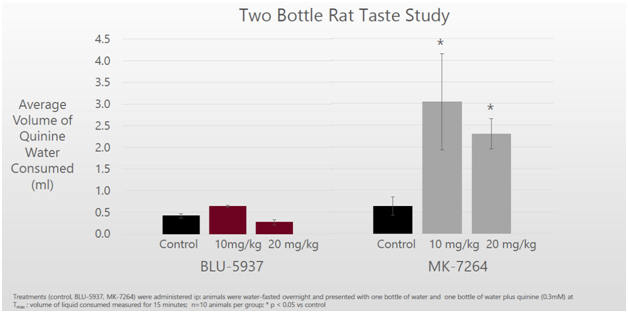

On the taste front, mice taking BLU-5937 were able to differentiate between regular water and quinine water (a bitter agent). Mice subjects consumed very little of the bottle with bitter quinine water when given the choice. On the other hand, mice given MK-7264 drank ~3-5 times more quinine water because they were not able to differentiate it from regular water. This can be explained by the loss of taste function.

Figure 4: Mice on BLU-5937 were able to distinguish difference between regular water and bitter quinine water. Mice on MK-7264 could not distinguish the difference due to taste loss and drank the quinine water.

Cell assay models showed that BLU-5937 was 40x more selective for P2X2/3 taste receptor in guinea pigs than MK-7264. This helps explain why mice in the preclinical study were able to distinguish between regular and quinine water. BLU-5937 inhibits the cough receptors but not the taste receptors. In humans, the company has said that BLU-5937 is 2000x more selective than MK-7264, so the taste effect should be even more pronounced.

Bellus will announce Phase 1 data in Q4 2018 (we expect December), which will assess the safety and taste effect of BLU-5937 in humans. Preclinical data and assay findings lead us to believe that BLU-5937 has a good shot of showing minimal taste disturbance in Phase 1 studies.

Key takeaways:

- Merck’s candidate has validated the mechanism of P2X3 drug class. BLU-5937, a P2X3 inhibitor, has shown early signs of being as effective at reducing cough.

- In vitro data has established that BLU-5937 is 40x more potent and 2000x more selective than MK-7264. This suggests that BLU-5937 may prove to be as effective at reducing cough in humans while showing no taste disturbance. If this holds true, BLU-5937 would be positioned as the best P2X3 drug in chronic cough.

Bottom Line: We believe there is a strong likelihood that Bellus’ Phase 1 taste data is positive. The difference in taste effect was evident during preclinical studies, and assays show that in humans, the drug’s effect can be even more distinguished.

Bellus is Worth At Least $1.25 if Phase 1 Data is Positive

Chronic cough is prevalent in ~10-12% of the population. It is estimated that ~1% of cases are unexplained, refractory chronic cough. In the US, this represents 2.6 million people. We assume treatment cost is $300/month, as per company guidance. Treatment periods in clinical studies run for about 3 months. Using these assumptions, we estimate the market opportunity is roughly $2.3 billion (2.6 million people*$300/month*3 months).

This market figure is supported by the high valuations that competing chronic companies have received, even though they’ve been early in development and presented little data supporting their candidates.

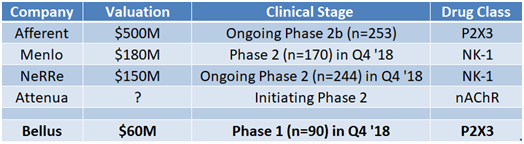

For example, NeRRE raised ~$30 million in their most recent Series B round at an estimated $150M valuation. NeRRe has presented an open label Phase 2 study that showed a 28% reduction in cough. Similarly, Menlo (MNLO) is expecting to present their first in-human data later this year, yet trades at a $180 million market cap. Attenua is initiating a proof of concept Phase 2 mid-year 2018 and the company was able to raised $35 million from bio-focused venture funds (valuation not disclosed). Afferent was on the verge of presenting late stage Phase 2b data, which ended up validating the P2X3 class as the most promising, when they were taken out by Merck for $500 million upfront.

These cases lead us to believe that if Bellus presents positive Phase 1 data this upcoming Q4, the company can warrant a $150 million valuation (or $1.25/share). This is 65% higher than current market price.

Figure 5: Bellus trades at a fraction of other chronic cough companies, even with a candidate in a class that has shown the most promise

Merck Has Paved the Path, Which May Shorten Development Time for Bellus

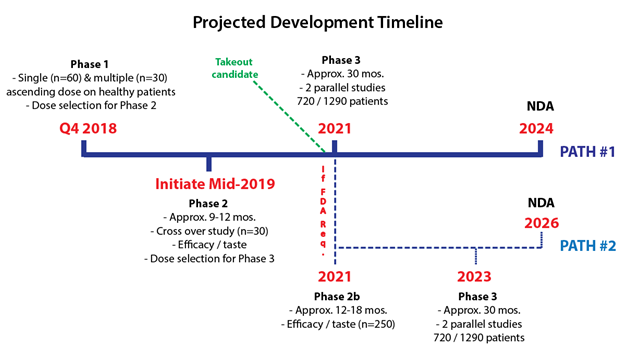

Bellus has been transparent with their development path and timeline. The company will follow the same path that Merck’s P2X3 candidate took, going head to head to demonstrate its best in class potential.

Following their Phase 1 in Q4 2018, Bellus plans to initiate a proof of concept Phase 2 in mid-2019 that will test efficacy/taste in about 30 patients. This study will follow the same design as Afferent’s study and will take approximately 9-12 months to readout (~mid-2020).

Post proof of concept Phase 2, Bellus will either go onto pivotal Phase 3 or be required to run a larger Phase 2b study. Merck’s candidate took the longer Phase 2b & Phase 3 route, presumably because it was the first P2X3 drug this far into development. Given the mechanism of P2X3 drugs has been validated by Merck, we believe Bellus may go directly to Phase 3, saving approximately 2 years.

Figure 6: BLU-5937 can get to market by 2024, but we believe exit can be much sooner

Bellus has made it apparent that the company’s first option will be to get acquired once BLU-5937 has been validated. On a call with PropThink (transcript here), CEO Roberto Bellini commented, “Primary exit strategy is to exit through an acquisition of the company post Phase II. We think that's the right timing for the company to get acquired by a big pharma.”

We anticipate that Bellus will report approximately CAD$17 million of cash by September 30, 2018. The Company has disclosed in presentations that this money will provide runway until 2020, subsequent to completion of Phase 2 proof of concept studies. We think that if Phase 1 data in Q4 2018 is strong, however, Bellus will complete an institutional financing and uplist to a national exchange such as the NASDAQ or NYSE. During this time, we think Bellus may be primed as a takeout target.

Bellus Boasts Concentrated Group of Investors:

- 35% owned by healthcare specialized institutional investors

- 30% owned by two family offices

Nearly all of Bellus’ institutional investors subscribed to the company’s December 2017 round, where CAD$20 million was raised. This financing caught our attention for several reasons. First, it was priced at an 8% discount to market at the time and was a clean offering with no attached warrant. Second, we were impressed at the quality of healthcare funds that participated in financing a preclinical stage Canadian biotech. We were able to discuss the investment thesis with a few of these U.S. institutional investors, who chose to remain anonymous for disclosure purposes, and share their sentiment on BLU-5937 upside.

Additionally, one of Bellus’ largest shareholders is their Chairman Francesco Bellini. Dr. Bellini was founder and CEO of BioChem Pharma, which was acquired by Shire in a deal valued at over $4 billion back in 2000. To this day, BioChem remains Canada’s largest biotech M&A deal. We think Dr.Bellini’s involvement and position as a biotech mogul will open many doors for Bellus moving forward.

Risks Mitigated By Large Target Market & P2X3 Mechanism

Competitive threats

Above we discussed the 4 main drug classes vying for chronic cough treatments. Many of these treatments are at similar stages of development (or more advanced) than Bellus. Refractory chronic cough (duration longer than 1 year) is estimated to be a multi-billion dollar market with no proven treatment. The market is large enough for multiple entrants. If we consider chronic cough (duration longer than 8 weeks), this market size can be as much as 10 times larger.

We’ve noted that the P2X3 drug class has shown the most clinical validation. Merck’s P2X3 candidate is the furthest advanced and has demonstrated the greatest efficacy in reducing cough. The other drug classes are early in development (nAChRs) or have reported sub-par data (TRP modulators and NK-1 antagonists).

How BLU-5937 will translate into humans

So far, BLU-5937 has been supported by cell assay models & preclinical data so naturally upcoming human data bears uncertainty. In theory, Bellus’ candidate should have the same mechanism as Merck’s P2X3 drug. Assay and preclinical data support this. This makes us confident that mechanism will translate over to human data. However, certainty is not given until data is actually presented.

Bellus’ upside offers investors a 65% return from current levels

We believe Bellus is burdened by legacy issues and lack of exposure. The company came off a public Phase 3 fail in AA amyloidosis in 2016 and lost about 90% of its value. The stock is currently trading little liquidity on the TSX/OTC markets, where Canadian biotech companies are generally overlooked. With an inflection point by year end, we think Bellus will become a prevalent name amongst the biotech crowd.

One or more of PropThink's contributors are long BLUSF.

Disclaimer: Use of PropThink’s research is at your own risk. You should do your own research and due diligence before making any investment decision with respect to securities covered herein. You should assume that as of the publication date of any report or letter, PropThink, LLC (possibly along with or through our members, partners, affiliates, employees, and/or consultants) along with our clients and/or investors (collectively referred to as “PropThink”) has a position in all stocks (and/or options of the stock) covered herein that is consistent with the position set forth in our research reports. When a contributor writes about a stock in which he or she holds a position, this is disclosed at the end of the article/research. Following publication of any report or letter, PropThink intends to continue transacting in the securities covered therein, and we may be long, short, or neutral thereafter regardless of our initial recommendation. Contributors and writers may not transact in the security covered therein in the two market days following publication. PropThink, LLC is not registered as an investment advisor. To the best of our knowledge and belief, all information contained herein is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable , and not from company insiders or persons who have a relationship with company insiders. On May 23, 2018, PropThink hosted a Digital Conference sponsored by Bellus Health Inc. PropThink was paid fifteen thousand dollars to organize, market and host this Digital Conference. PropThink's full disclaimer is available at http://propthink.com/disclaimer

Access This Content Now

Sign Up Now!