Zogenix (ZGNX) will be releasing data from its pivotal Phase 3 program of ‘ZX008’ intended for the treatment of Dravet Syndrome (DS), a form of early-onset epilepsy in ‘late Q3’. ZX008 is ZGNX’s lead and only candidate. For this reason, we are expecting elevated volatility. We want to profit from this event and the best way to do so, in our view, is to sell calls and puts to take advantage of the elevated premium for these options. Here’s what we’re doing to play Zogenix:

- Selling $21 October 20, 2017 Calls for $4.00

- Selling $10 October 20, 2017 Puts for $3.80

Summary of Trade

We will collect approximately $7.80 in premium by selling the calls and puts outlined above. This means our ‘profit-range’ is anywhere between $2.20 and $28.80. If ZGNX trades below $2.20 or above $28.80, we lose. Our best case scenario, where we keep the whole premium, is for ZGNX to end up between $10 and $21.

How Does This Work (Skip This Part If You’re Familiar With Options)

When you sell an option, you become obligated to the buyer in a certain regard. For instance, if you sell the puts at $10 expiring October 20, you will, at any time and until October 20, be obligated to buy ZGNX common shares at $10 a share. For this obligation, the buyer of the option will pay you $3.80 or so (depending on the bid/ask and actual transaction price) for each option contract. In essence this means that if shares of ZGNX stay above $10, it is DEFINITELY unprofitable for the buyer of the option to ‘put’ you shares underlying those options you sold. In reality, you brought in $3.80 in cash, which means your cost basis on those shares is really $10 (the strike) minus $3.80 (the premium you collected) which equals $6.20 a share.

What Happens if Zogenix Reports Good Data?

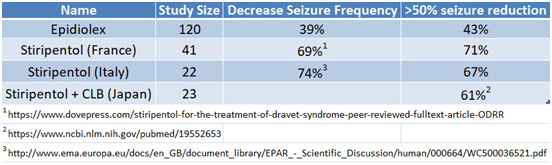

In the past, ZX008 has shown to reduce seizure frequency by >50% in about 70% of patients, albeit on a small population n=19. For comparison, GW Pharma’s Phase 3 study of Epidiolex (cannabidiol) in Dravet syndrome showed a 39% reduction in median seizure frequency between baseline and 43% of patients experienced a ≥50% reduction in seizure frequency. Stiripentol has been approved in Europe, but not in the US, for Dravet Syndrome and has shown reduction rates between 60-70%, shown below.

What Happens if Zogenix Reports Good Data?

In the past, ZX008 has shown to reduce seizure frequency by >50% in about 70% of patients, albeit on a small population n=19. For comparison, GW Pharma’s Phase 3 study of Epidiolex (cannabidiol) in Dravet syndrome showed a 39% reduction in median seizure frequency between baseline and 43% of patients experienced a ≥50% reduction in seizure frequency. Stiripentol has been approved in Europe, but not in the US, for Dravet Syndrome and has shown reduction rates between 60-70%, shown below.

Zogenix’s September data will be a double-blinded, randomized, controlled 12-week study with n=120 patients. If ZX008 is able to replicate prior results, ZGNX will make a strong case for being a leading DS treatment and superior drug to GWPH’s cannabidiol.

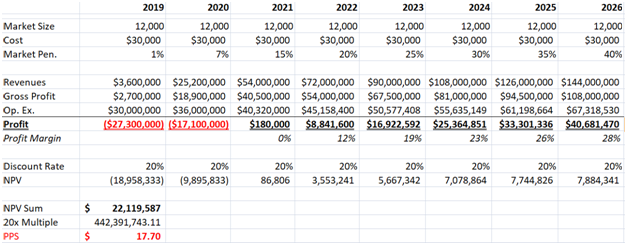

We estimate the US and European population for DS to be 12,000 patients and for ZX008 to price at $30,000. This means a total market size of $360 million. We project peak sales to be around $145M in 2026 under our best case scenario (as shown in the table below). A back of the envelope valuation leads us to a price per share of $18, if ZGNX presents good data. Our assumptions are included in the table.

We estimate the US and European population for DS to be 12,000 patients and for ZX008 to price at $30,000. This means a total market size of $360 million. We project peak sales to be around $145M in 2026 under our best case scenario (as shown in the table below). A back of the envelope valuation leads us to a price per share of $18, if ZGNX presents good data. Our assumptions are included in the table.

When modeling the upside for ZGNX on positive data results, we took into consideration fenfluramine’s (ZX008 compound) history of cardiac side effects in other indications. Fenfluramine was used in the combination drug fen-phen, which was marketed for weight loss and eventually pulled from the market due to its potentially fatal pulmonary hypertension and heart valve defects.

ZGNX has not reported any cases of pulmonary hypertension in its studies, but two patients saw a slight thickening of one or two heart valves. In both patients, these findings were not considered clinically significant and neither patient stopped therapy. However, only a small patient population of 20 was examined. In a 120 patient study, the safety profile could differ significantly, which is why we are aggressive when valuing ZGNX upside.

Moreover we couldn’t care less how much ZGNX sells. We simply wanted to understand the best strike to sell calls at. This work supports our thesis that selling $21 Oct calls is prudent. Let the buyer take the tail-end outcome. Selling these options means we win in all but one scenario, kind of like ‘the house’ in a casino.

What Happens if Zogenix Reports Bad Data?

If ZX008 fails to meet its designated endpoint, ZGNX could trade down to a Q3 pro-forma cash balance of ~$52 million (per share basis of ~$2.10). Zogenix would have to turn to their second ZX008 study (Study 1504), which looks at ZX008 as a combination with other treatments stiripentol, valproate, and clobazam. This strategy option offers us protection on the downside until $2.20, although we think that the probability of a drop lower than [2.20] is highly unlikely.

Zogenix has powered their upcoming study to reach a 40% difference in baseline between active and placebo arms, higher than the 26% variance GWPH reported. Management considered this expected variance as “rather conservative” and prior studies are in the 55%-65% range.

The company expects to report the second ZX008 study (Study 1504) in Q1 2018, which combines ZX008 with other treatments stiripentol, valproate, and clobazam, giving the them a “Plan B” in case monotherapy does not pan out.

Risks

The short strangle leaves us exposed if ZGNX trades lower than $2.20 or higher than $28.20. We think either case is a long shot. On the downside, we think the trial design implies that a complete disaster has a tail end probability.

On the upside, Zogenix has to replicate its prior results and report a clean safety profile for the stock to potentially trade above $28. We think the likelier outcome is the company reporting better than expected results with efficacy but some lingering safety questions that will keep a lid on shares in and around the range of $18.

ZGNX has not reported any cases of pulmonary hypertension in its studies, but two patients saw a slight thickening of one or two heart valves. In both patients, these findings were not considered clinically significant and neither patient stopped therapy. However, only a small patient population of 20 was examined. In a 120 patient study, the safety profile could differ significantly, which is why we are aggressive when valuing ZGNX upside.

Moreover we couldn’t care less how much ZGNX sells. We simply wanted to understand the best strike to sell calls at. This work supports our thesis that selling $21 Oct calls is prudent. Let the buyer take the tail-end outcome. Selling these options means we win in all but one scenario, kind of like ‘the house’ in a casino.

What Happens if Zogenix Reports Bad Data?

If ZX008 fails to meet its designated endpoint, ZGNX could trade down to a Q3 pro-forma cash balance of ~$52 million (per share basis of ~$2.10). Zogenix would have to turn to their second ZX008 study (Study 1504), which looks at ZX008 as a combination with other treatments stiripentol, valproate, and clobazam. This strategy option offers us protection on the downside until $2.20, although we think that the probability of a drop lower than [2.20] is highly unlikely.

Zogenix has powered their upcoming study to reach a 40% difference in baseline between active and placebo arms, higher than the 26% variance GWPH reported. Management considered this expected variance as “rather conservative” and prior studies are in the 55%-65% range.

The company expects to report the second ZX008 study (Study 1504) in Q1 2018, which combines ZX008 with other treatments stiripentol, valproate, and clobazam, giving the them a “Plan B” in case monotherapy does not pan out.

Risks

The short strangle leaves us exposed if ZGNX trades lower than $2.20 or higher than $28.20. We think either case is a long shot. On the downside, we think the trial design implies that a complete disaster has a tail end probability.

On the upside, Zogenix has to replicate its prior results and report a clean safety profile for the stock to potentially trade above $28. We think the likelier outcome is the company reporting better than expected results with efficacy but some lingering safety questions that will keep a lid on shares in and around the range of $18.

One of more of PropThink's contributors have sold $18 October 20, 2017 Calls for $3.00 & $10 October 20, 2017 Puts for $4.20.

UPDATE: ZGNX rallied on 9/6/2017 so we updated the options trade from:

- Selling $18 October 20, 2017 Calls for $3.00

- Selling $10 October 20, 2017 Puts for $4.20

TO:

- Selling $21 October 20, 2017 Calls for $4.00

- Selling $10 October 20, 2017 Puts for $3.80

Access This Content Now

Sign Up Now!