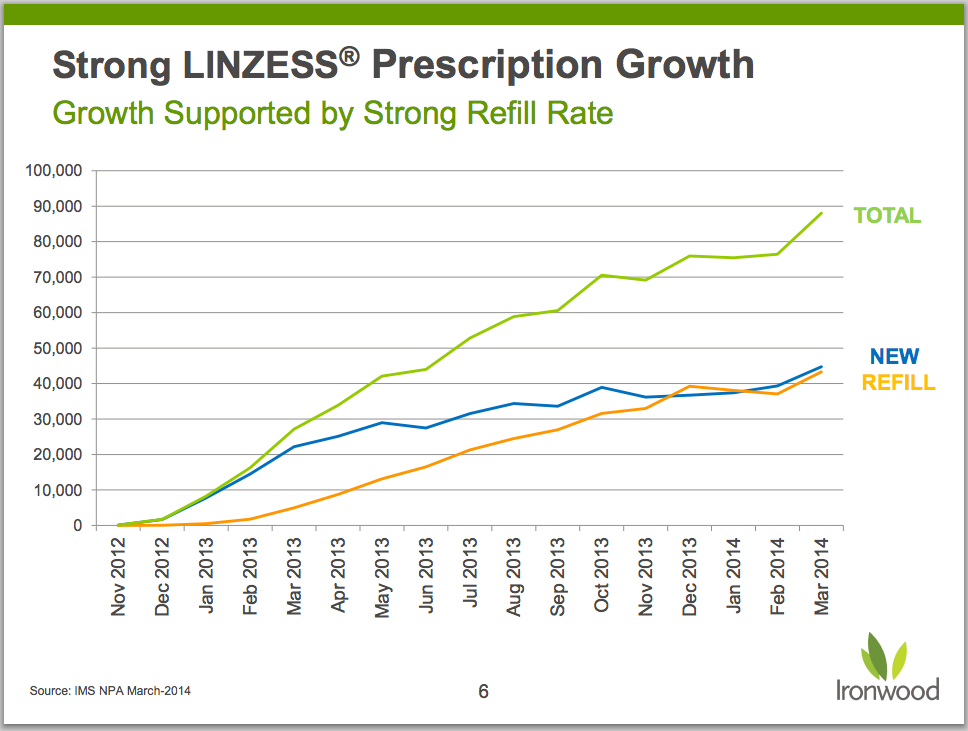

- Refill rates and total prescriptions for Linzess continue to track positively. Advertising campaign, which began last month, should have a meaningful impact on script rates – and Linzess sales.

Ironwood Pharmaceuticals (IRWD) closed the day up 11% following revenue and earnings beats in the first quarter as sales of the company’s only approved and marketed product, Linzess (linaclotide), continue to grow. Linzess is approved for Irritable Bowel Syndrome with Constipation (IBS-C) and Chronic Idiopathic Constipation (CIC). This latest suggests Linzess is producing a loyal patient base as refill rates track new prescription trends. And with a major advertising program getting off the ground, we suspect the next few quarters will be good for Linzess sales.

Ironwood and partner Forest Labs (FRX) reported Linzess sales of $60.8 million (a run rate of $243.2M) in the first calendar quarter (Forest’s fiscal fourth quarter), a 19% improvement over the previous quarter. Ironwood and Forest jointly fund the development and commercialization of Linzess, splitting equally net profits/losses on the product. Ironwood booked revenue of $14.6M in 1Q14, $8.4M from its profit split with Forest and $6.2M from API sales & milestone/royalties from overseas partnerships. Ironwood reported a net loss of $49.6 million, or $0.38 per share.

Importantly, new prescriptions and refills continue to climb in parallel.

At just under 240,000 prescriptions filled in the quarter, Linzess prescriptions were up 11% sequentially. New prescriptions and refills trending higher in tandem are encouraging since Linzess has taken some flack for high rates of diarrhea (20% in IBS-C trials, 16% in CIC trials). It would be disconcerting to see refill rates breaking away significantly from new prescriptions (i.e. “tried it, don’t like it”).

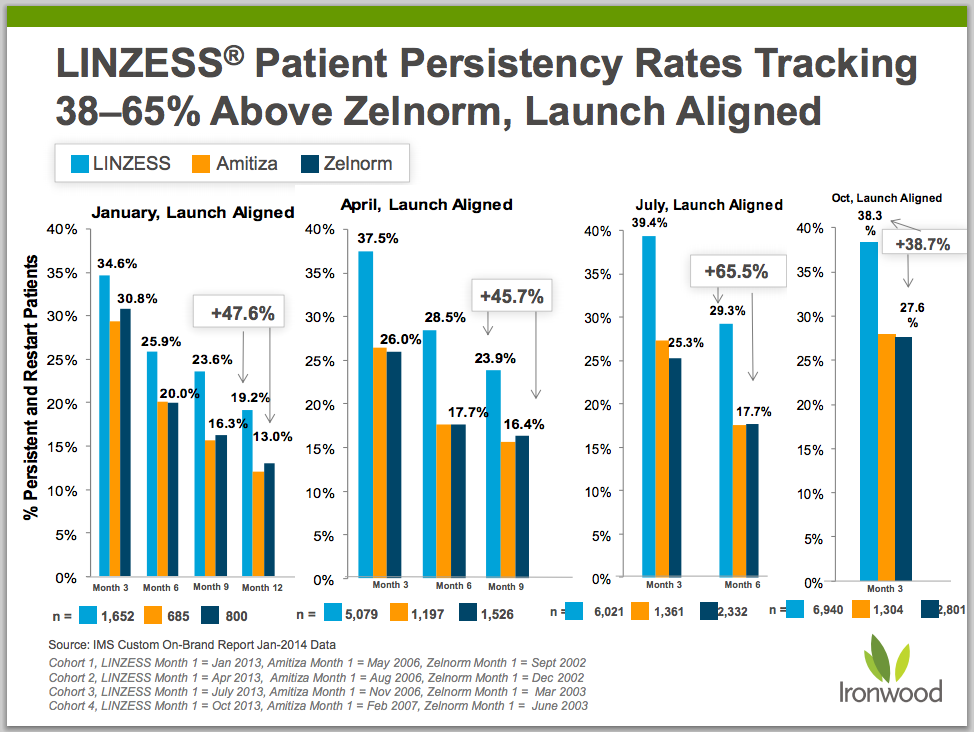

Patient persistency rates also signal a sticky patient base. Linzess persistency is tracking ahead of Zelnorm (tegaserod), a decent proxy for Linzess’ potential, in the months since launch. Zelnorm was heralded in the early 2000’s as the next blockbuster treatment for IBS-C and CIC. In 2006, there were more than 16 million prescriptions written for Zelnorm, with sales totaling $560M. The ramp was stopped short, however, when Zelnorm was pulled from the market (2007) due to concerns over possible adverse cardiovascular effects.

Ironwood kicked off a Direct-to-Consumer advertising campaign (TV, digital) in the second week of April which should make itself apparent in prescription rates over the next 3-6 months. Given the ramp seen with Zelnorm when a focused advertising campaign started, and the nature of the target population, marketing efforts should have a meaningful impact on prescription rates for Linzess – and, of course, sales. For a back of the envelope look at Linzess’ potential, we use a price per prescription of $196.35 ($7.70/day with a 25% gross to net discount). At half of the 16 million prescriptions that Zelnorm did in 2006, sales would top $1.5B. This is why Ironwood currently carries a lofty $1.5B valuation, and why analysts have been calling for sales multi-billion dollar peak sales. D

Driven by prescription trends and the direct-to-consumer campaign, IRWD’s second and third quarters will be interesting, and we’re optimistic about the stock if the macro situation holds up. On a related note, Synergy Pharmaceuticals (SGYP) will have phase 2 data for its own guanylate cyclase-C agonist, plecanatide, any day. We’ve opined extensively on SGYP, plecanatide, and the relation to Ironwood in the past.

One or more of PropThink’s contributors are long SGYP.