2013 has been a banner year for biotech IPO’s, with a number of companies making their public debuts to strong reception by the market. BIND Therapeutics (BIND), founded in May of 2006 and public since September 2, of 2013, has a solid balance sheet post-IPO, a novel approach to treating cancer, and a slate of blue-chip partnerships signed on favorable terms. Although its post-IPO performance has been muted, investors can own the stock at current levels ahead of several analyst & investor events in October, as well as the initiation of sell-side coverage shortly thereafter. Overall, BIND’s Accurin platform is a novel approach in targeted therapeutics, and while the valuation is a little steep given the sparse human data, we’re comfortable holding the stock ahead of 2014, an important year in datapoints.

Overview

BIND’s oncology candidates are anchored by a novel nanomedicine platform based on Accurins, the company’s line of “programmable” therapeutics. These Accurins are designed to maximize the level of drug delivered to a patient while minimizing potential side effects. Specifically, Accurins contain four distinct features (as defined by BIND) that set them apart from existing standards of treatment and drug delivery systems.

-

“Targeting ligands”: BIND has designed Accurins to be able to bind (hence the name of the company) to a variety of cell-surface and/or tissue markers, based on peptides, molecules, and antibody fragments. This allows Accurins to be adapted to different types of cancers.

-

“Stealth and protective layer”: Accurins utilize polyethylene glycol (also known as PEG), which allows long-term distribution throughout a patient’s circulatory system.

-

“Polymer matrix”: BIND’s Accurins are not actually a new class of drugs per se. Rather, the company seeks to incorporate existing oncology drugs and improve upon their delivery, efficacy, and safety. To that end, each “Accurin” contains a predetermined dose of an existing cancer drug, which is contained in a biodegradable polymer matrix that is programmed to release the drug at a pre-specified rate.

-

“Therapeutic payload”: This fourth and final aspect of BIND’s Accurins is perhaps the most important. By their very nature, Accurins are able to accept and deliver a wide range of drugs, such as small molecules, mRNA, and proteins. This allows for the potential use of Accurins in markets beyond oncology.

In studies of rats treated with Accurin-based Oncovin (vincristine), BIND detected Oncovin concentrations over 100x higher than in rats that were given Oncovin via conventional methods, highlighting the ability of Accurins to accumulate in a patient’s system. And in monkeys, Accurin-based Oncovin was given with minimal side effects at doses that have been documented to be fatal in cynomolgus monkeys. BIND has also tested Accurin-based Oncovin in cancerous mice; the data showed that 1 dose of Accurin-based Oncovin inhibited tumor growth for 50 days after treatment, versus the 2-week inhibition noted for conventionally administered Oncovin. Similarly, positive results were recorded with the use of Accurin-based Velcade (bortezomib). In pre-clinical mouse models of human lung cancer, Accurin-based Velcade was able to suppress tumor growth rates, while conventional Velcade had no effect (we note Velcade is approved for the treatment of multiple myeloma and relapsed mantle cell lymphoma).

BIND is already in the process of testing an Accurin-based oncology treatment in the clinic and has inked collaboration agreements with three blue-chip pharmaceutical and biotechnology companies.

BIND-014: Taxotere With A Twist

BIND-014 is a PSMA-targeted Taxotere (docetaxel) Accurin now in Phase II trials for the treatment of prostate and lung cancer. Docetaxel is approved by the FDA to treat breast cancer, NSCLC, gastric cancer, head and neck cancer, and prostate cancer. Existing data for BIND-014 has been encouraging, both from a safety and efficacy perspective. Pre-clinical studies of BIND-014 across several animal species suggested acceptable safety and efficacy, as well as a differentiated pharmacokinetic profile relative to conventional docetaxel. In cynomolgus monkeys that were treated with BIND-014 and monitored for 70 hours, concentrations of BIND-014 were, at a minimum 10x higher than conventional docetaxel, with concentrations climbing to as high as 100x at the start of monitoring. In prostate cancer mouse models, BIND-014 also demonstrated favorable concentrations, as shown in the graph below.

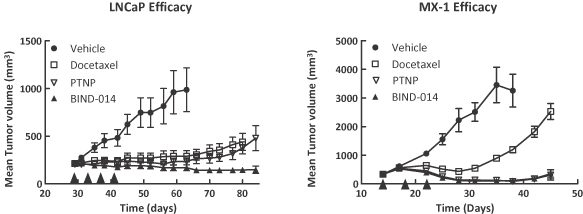

We note that there was no statistically significant difference in concentrations at 2 hours after administration, but that concentrations of BIND-014 increased materially over the next 10 hours, versus a material decline in conventional docetaxel, leading to significantly (p<0.01) higher concentrations over time. To test the efficacy of BIND-014, BIND implanted prostate (from the LNCaP cell line) and breast cancer (from the MX-1 cell line) tumor cells into mice and split them into four separate groups: mice treated with docetaxel, PTNP (a modified version of BIND-014 without its PSMA targeting ligands), BIND-014, and placebo. The mice were dosed with one of these treatments every four days, with breast cancer mice receiving a total of three doses and prostate cancer mice receiving a total of four doses. This pre-clinical study concluded that BIND-014 led to statistically significant shrinkages in tumors relative to docetaxel in both tumor models (p<0.05 in prostate cancer, p<0.01 in breast cancer). The use of PSMA targeting was also validated by this model, as conventional BIND-014 showed statistically significant (p<0.05) superiority relative to PTNP in the prostate cancer model, but yielded equivalent efficacy in breast cancer, which does not express PSMA. The efficacy of each of these four treatment arms is summarized below.

Although BIND runs two Phase II trials in prostate and lung cancer, BIND is also conducting a Phase I trial (NCT01300533) of BIND-014 in patients with a variety of advanced or metastatic cancers, specifically those for which there is no “standard or curative therapy” as defined in the trial’s inclusion criteria. The trial is split into two dosing arms, Q3W and Q1W, and BIND has already completed the Q3W arm; the Q1W arm portion of the trial is ongoing. Results from the Q3W dosing arm (with a total of 30 patients, each of whom previously failed existing standards of care) showed that BIND-014 was fairly well tolerated. 25 patients experienced a treatment-related adverse event, and three patients discontinued treatment. There was one death in the trial; an elderly patient with advanced biliary cancer as well as a biliary stent that contracted sepsis as a result of neutropenia. We remind investors that neutropenia is a documented side effect of docetaxel, and that the neutropenia experienced by patients in the Q3W trial arm was due to underlying systemic exposure to docetaxel. We also note that this patient was dosed with a 75 mg/m2 dose of BIND-014, and BIND has determined that 60 mg/m2 is the maximum tolerated dose, versus a typical 75 mg/m2 dose when conventional docetaxel is used.

This Phase I trial also assesses preliminary indications of efficacy. In the Q3W arm, 28 patients were evaluable for efficacy. Of these, there was one complete response in cervical cancer and three partial responses in patients with prostate, lung, and ampullary cancer. In addition, five other patients had stable disease of at least 12 weeks. The Q1W portion of the trial is currently ongoing. Multiple sources, including both existing docetaxel clinical data and BIND’s own pre-clinical studies, have shown that Q1W dosing leads to a lower rate of neutropenia and that higher exposure to docetaxel may yield favorable efficacy relative to Q3W dosing. As of late August, a total of 26 patients have been enrolled in the trial, and 45 mg/m2 has been the highest dose tested.

Two Phase II trials evaluate BIND-014 in both prostate and lung cancer. In the first trial (NCT01812746), BIND tests BIND-014 in chemotherapy-naïve prostate cancer patients (specifically metastatic castration-resistant prostate cancer), and will enroll a total of 40 patients. With a primary completion date of August 2014, the trial takes a closer look at efficacy (rPFS, radiographic progression-free survival) and safety. The second trial (NCT01792479) tests BIND-014 as a 2nd-line therapy in patients with non-small cell lung cancer and will also enroll a total of 40 patients. The trial, which wraps up late next year, will also evaluate both efficacy (measured by objective response rate) and safety.

BIND notes that its preliminary discussions with the FDA suggest that BIND-014 may ultimately qualify for 505(b)(2) status, an expedited and simpler approval process given the drug’s similarities to decetaxel. BIND-014 also appears to be protected by a decent patent portfolio, with 6 issued patents (five in the United States and one in Europe), as well as 16 pending domestic patents. BIND’s issued patents offer protection through 2025-2030, and the company’s pending applications may extend protection as far as 2034.

Existing data for BIND-014 suggests that it has potential to offer a new approach to treating lung and prostate cancer, and with possible 505(b)(2) status, BIND’s pathway to commercialization may be shorter than that of many other biotechnology companies. Furthermore, we note that BIND, despite having multiple collaborations in place, the company retains full rights to the asset.

Collaboration Agreements: Free R&D is Always Welcome

BIND has three separate collaboration agreements in place, all of which were signed in 2013. In January, the company inked an agreement with Amgen (AMGN), followed by an agreement with Pfizer (PFE) in March, and AstraZeneca (AZN) in April. Each of these agreements came with small upfront payments and hundreds of millions in milestone payments.

-

Amgen: BIND received $5 million upfront when it inked its deal with Amgen, which grants Amgen the option to license an Accurin developed around a specific Amgen kinase inhibitor. Amgen has until January 2014 to exercise the option, after which BIND is then granted the option to secure an exclusive license from Amgen for said kinase inhibitor. Should Amgen exercise its option, BIND will receive an additional $111.5 million (assuming Amgen licenses this Accurin for development in two indications), and will be eligible for up to $188 million in additional commercial milestone payments, as well as mid-single digit to low-double digit royalties on global sales of this kinase-based Accurin. Furthermore, should Amgen exercise its option, it will be responsible for paying all external expenses relating to its agreement with BIND, as well as for the payment of “certain development costs.”

-

Pfizer: BIND received $4 million upfront when it signed its agreement with Pfizer in exchange for granting the company a 30-month option to exclusively license Accurins for all potential indications other than vaccines and brain cancer. Should Pfizer exercise its option, it will pay BIND an undisclosed option fee, and BIND will receive up to $89.5 million in clinical and regulatory milestones, as well as up to $110 million in commercial milestone payments. In addition, BIND will receive low to high single digit royalties on global sales of any licensed products, and Pfizer must pay all development costs related to its agreement with BIND.

-

As in the deal with Pfizer, AstraZeneca will pay all of BIND’s development costs related to this collaboration. Unlike the Amgen and Pfizer agreements, this agreement is not based on an option; AstraZeneca has already secured a global license to develop Accurins based on AstraZeneca compounds. BIND received $4 million upfront and is eligible for up to $193 million in milestone payments (covering clinical, regulatory, and commercial milestones), as well as low-single digit to low-double-digit royalties.

The vast majority of the development costs related to these agreements will not be paid by BIND; the company can sit back and collect milestone payments, which the company notes reach over $1 billion, exclusive of any potential royalty payments (we note that the payments listed above total $705 million; BIND has not disclosed the specifics of the remaining milestone payments). Management expects that by the end of 2014, at least one of these three programs will begin clinical trials, and we note that AstraZeneca is already preparing an IND. The capital BIND is eligible to receive from these three agreements gives the company incremental resources with which to develop its own pipeline, which contains two additional solid tumors and hematologic programs.

Financials & Insiders

On a pro forma basis, BIND ended Q2 2013 with $79.791 million in cash & equivalents (inclusive of $4.208 million in debt), versus a market capitalization of less than $236 million (based on 15,777,322 shares outstanding and an October 5 closing price of $15), around $294 million on a fully diluted basis when adjusting for potential shares issued under BIND’s employee stock plans and the conversion of BIND’s remaining preferred stock (which would bring its share count to 19,658,913). BIND’s historical burn rates of $17.238 million in 2012 and $13.025 million in 2011 suggest that the company’s present cash balances are sufficient to fund operations for some time; even with an increase in its burn rate to $25 million, BIND has three years of capital on its balance sheet, not accounting for milestone payments related to its collaboration agreements.

In addition to a decent balance sheet, BIND’s largest investor class is its management team and board of directors. Together, they own a total of 5,367,240 shares, equivalent to 34.02% of BIND’s currently outstanding shares, or 27.3% on a fully diluted basis. In addition, BIND’s largest institutional shareholder, Polaris Ventures, owns 12.63% of the company (and around 10% on a fully diluted basis). Polaris’ general managing partners, Amir Nashat, also sits on BIND’s board of directors. The same is true of BIND’s #2 shareholder, Flagship Ventures (with a current stake of 9.78%, or 7.85% on a fully diluted basis), whose CEO and managing partner also sits on BIND’s board of directors. Together, BIND’s insiders and top two institutional investors, both of whom are affiliated with BIND’s board, control over 56% of the company’s existing shares, and over 45% on a fully diluted basis. In our view, this level of insider ownership aligns the interests of management and the company’s board quite well with that of outside investors.

Catalysts & Conclusions

Like Stemline Therapeutics (up over 200% since our May 24 report), BIND’s current float is well below its outstanding sharecount given the sizable stakes held by institutional shareholders and insiders. Initiation of analyst coverage (BIND’s IPO was conducted by Credit Suisse, Cowen, JMP, and Stifel) are likely to put fresh eyes on the stock, as well as a set of investor events scheduled for October. On October 10, BIND will be presenting at the Partnerships in Drug Delivery Conference, and on October 18 the company will be hosting a nanomedicine day in New York to highlight its Accurin platform. Both events will raise BIND’s profile in the investor and medical communities and may help spark a rise in the company’s stock price.

With a well-capitalized balance sheet, a slate of collaboration agreements, and a management team and board that own a majority of the company’s existing shares, BIND is well-positioned to advance its Accurin platform. Ahead of analyst coverage launches and several investor events, we’re initiating a small position, keeping powder dry to revisit this story next year as mid-stage studies read out. While the Accurin platform is still early in human testing, BIND’s targeted therapeutic approach has certainly piqued our interest.