- The regulatory and legislative environment has improved dramatically in the last half-decade for antibiotics developers, with some new incentives still in the works, and we continue to see CBST as a must-own in the mid-cap biopharma space for longterm investors.

- Stock has been battered along with the sector, but the name should get credit for a P&L focus and deeper pipeline than other small-cap development-centric biotech stories.

One of the pharmaceutical industry’s major themes over the past dozen years has been the abandonment of antibiotics development as one company after another shifts focus to more profitable facets of the market. Meanwhile, a new crop of small companies dedicated to the development of novel anti-infective therapies has rushed to fill the void. Of the publicly traded players, mid-cap Cubist Pharmaceuticals (CBST) leads the pack, and smaller players like Cempra (CEMP) or Tetraphase (TTPH) are set to benefit from what we believe will be increasingly favorable regulatory environment over the next few years.

The FDA has gone lengths to incentivize the development of next-generation antibiotics. Coupled with recent moves in Congress, the landscape for antibiotic developers should only become more favorable over the next two to three years as legislative and regulatory participants move to stem the prevalence of highly resistant bacteria.

The stage is set for Cubist to continue expanding its position as the leading pure-play antibiotics company, and it’s a story worth paying particular attention to as development-centric small-caps take the brunt of the current slump in biotech.

While CBST has returned less than 1% since our last report on December 30, the stock has slightly outperformed the NASDAQ Biotechnology Index (IBB). Cubist’s Q1 2014 results missed estimates, but the single quarter isn’t representative of the company’s potential.

PropThink readers can catch up on our previous coverage of Cubist here, and Cempra, Inc. (CEMP), here.

Incentivizing Antibiotics Development

With concern growing globally over the prevalence of drug resistant infections, and a general dearth of new antibiotics, legislators and regulators have moved to incentivize antibiotic development.

Those following the sector will be aware of these recent actions: in July of 2012, Barack Obama signed into law the Food and Drug Administration Safety and Innovation Act (FDASIA), legislation that both renewed the FDA’s authority to collect user fees and strengthened its ability to provide flexibility in the regulatory review process (breakthrough therapy designations, for example). Among the various provisions, the GAIN Act, or Generating Antibiotic Incentives Now, includes: extended regulatory exclusivity for new antibiotics; fast track and priority review status for therapies that meet GAIN standards; and increased communication/clinical guidance with drugmakers regarding the pathway for pathogen-focused antibiotics. GAIN has been manifest in several ways, perhaps most notably in the IDSA’s (Infectious Disease Society of America) 10 x ’20 initiative, which advocates for the approval of at least 10 new antibiotics by the year 2020.

Of publicly traded healthcare companies, Cubist leads the charge with two NDA’s pending before the FDA and a goal of being responsible for launching four of the IDSA’s ten targeted antibiotics by 2020 – pretty cool stuff.

But there are those in Washington that believe the landscape still isn’t robust enough, and there have been moves to provide even more “sweeteners” to the industry. Senator Sherrod Brown (D-OH) recently introduced the Strategies to Address Antimicrobial Resistance Act (the STAAR Act), which aims to strengthen the government’s focus on combating drug-resistant infections with an increased emphasis on research and inter-agency coordination (Department of Health & Human Services among others).

Further, the DISARM Act (Developing an Innovative Strategy for Antimicrobial Resistant Microorganisms), introduced in March 2014 in the House by Representatives by Peter Roskam (R-IL) and Danny Davis (D-IL), directs Medicare to increase reimbursement payments to hospitals that utilize novel antibiotics. The bill is being sold in Congress as revenue neutral, with the higher costs of reimbursement offset by shorter hospital stays and lower readmission rates. DISARM would also mandate a long-term and comprehensive study by the CDC, GAO, PTO, and FDA to “identify obstacles to a vibrant and competitive advanced antibiotics marketplace,” with a goal of further streamlining the antibiotics approval process and intellectual defenses. DISARM has the support of a wide swathe of the healthcare industry (of course), including IDSA, Merck (MRK), AstraZeneca (AZN), Forest Labs (FRX), and GlaxoSmithKline (GSK).

With the backdrop of a favorable regulatory and legislative environment, we find Cubist to be particularly noteworthy for its scale, pipeline, and the relative safety of a commercial operation.

Cubist’s Start to 2014

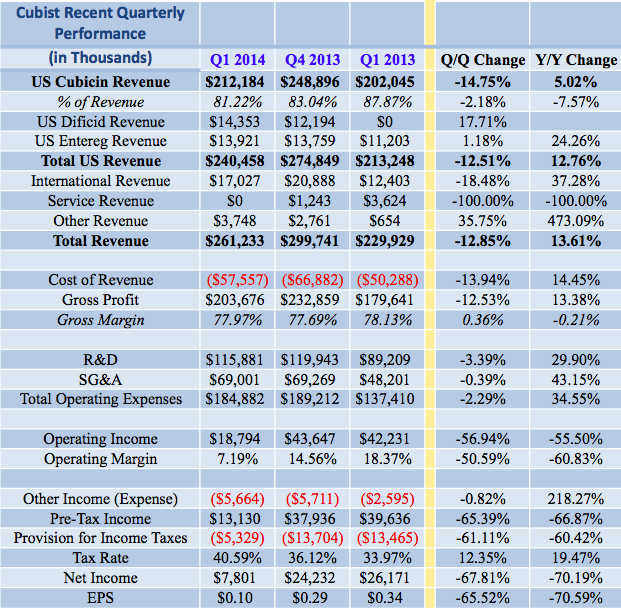

Cubist’s first quarter results were a continuation of the past several quarters: a sustained decline in operating profit and EPS amidst low double-digit revenue growth.

Nevertheless, the markets have been expecting this as Cubist integrates Optimer and Trius Therapeutics and ramps its R&D spend. We break down Cubist’s Q1 2014 results below.

Cubist posted total revenues of $261.23 million and EPS of $0.10, missing consensus by $24M and $0.23, respectively. The EPS miss can be attributed in-part to analysts’ treatment of the company’s CVR value reversal from the Trius/Optimer deals, which must be marked to market under GAAP (and which the company excludes from non-GAAP results).

Despite the misses, Cubist reaffirmed its full-year guidance, including net domestic Cubicin revenues of $1.19 – $1.275 billion.

Domestic Cubicin sales grew by just over 5% year over year in Q1 2014 (the sequential decline from Q4 was attributed to seasonality). While vials shipped were down 3.6% in Q1 2014 versus a year ago, Cubist’s market share has historically been adversely affected by the fact that the company does not offer pneumonia treatments. We don’t find the decline particularly alarming in light of the full year guidance affirmation, which suggests the company anticipated a soft quarter.

Of note is Cubist’s continued revenue diversification: in Q1 2014, domestic Cubicin sales accounted for 81.22% of total revenue, down over 6 percentage points year-over-year. Assuming Sivextro (tedizolid phosphate) secures regulatory approval, the percentage will continue to decline. International revenues (royalties on Cubicin sales) grew by over 37%, and Entereg (alvimopan) sales increased by over 24% year-over-year. We note that Cubist’s year-over-year revenue growth is skewed by both the addition of Dificid revenue (via the acquisition of Optimer) and the loss of service revenue tied to the company’s historical agreements with Optimer. Excluding these two revenue sources, Cubist’s revenue growth for Q1 2014 came in at 9.1%. We believe that Dificid revenues will improve over the course of 2014. With the closing of its takeover of Optimer, Cubist set about reshaping the Dificid sales force for an increased focus on CDAD patients. Cubist management alluded to an increase in positive physician feedback since February, and we expect the results of these sales force changes to become more noticeable through 2014.

Cubist posted decent revenue growth in Q1, with gross margins largely holding at around 78%, yet the company experienced a sharp drop in operating profits and EPS. This was largely expected. 2014 is transition year for Cubist as the company pushes two New Drug Applications and integrates Trius and Optimer; both acquisitions are currently dilutive to EPS.

R&D spending at Cubist surged almost 30% in Q1 2014. Operating profit was further pressured by SG&A deleveraging as a result of the acquisitions of Optimer and Trius, neither of which were profitable at the closing of their takeovers. Cubist is working to rectify this, and the company has affirmed that Optimer will become accretive to earnings by the end of 2014 as Cubist realizes operating synergies. Management said that the Optimer and Trius R&D teams have been fully integrated and that their SG&A integration is 85% complete, set to wrap up this quarter. Although analysts call for EPS of just $0.50 in 2014, consensus calls for earnings of $1.94 in 2015 as revenue growth accelerates to almost 20% with initial sales of Sivextro (PDUFA date of June 20). Cubist expects a commercial launch by the end of the year.

The Trius and Optimer acquisitions leveraged the company’s balance sheet, but Cubist ended Q1 2014 with $566 million in cash & investments ($826.25 million in convertible notes) due in three tranches in 2017, 2018, and 2020. Of further note are Cubists’ Net Operating Losses. The acquisitions of Trius and Optimer brought with them $475 million in net operating loss carryforwards that can be used to offset future taxes. Cubist has taken the now-common step to optimize its tax structure; ownership of the Sivextro patent portfolio has been transferred to Cubist’s international subsidiary to lower the overall tax burden.

The Year Ahead

2014 is a year of transition, though Cubist is poised to expand its franchise from three products (Cubicin, Dificid, and Entereg) to five.

Sivextro is under review at the FDA, with a PDUFA decision on June 20. An approval decision in Europe is slated for the first half of 2015. Physicians will get their first look at detailed Phase III data for ceftolozane/tazobactam in cUTI and cIAI at the 2014 European Congress of Clinical Microbiology and Infectious Diseases (ECCMID) this week. Trials testing ceftolozane/tazobactam in hospital-acquired/ventilator-associated bacterial pneumonia (HABP/VABP) will begin by the end of this quarter. Approval of ceftolozane/tazobactam in HABP/VABP will help fill Cubicin’s current market gap in pneumonia (an issue that contributed to Cubicin share-loss in Q1). Consensus calls for peak global sales of over $1 billion, and with patent protection through 2023 (European Union) and 2024 (United States), the therapy appears well-protected.

Cubist continues with progress on other pipeline assets: Surotomycin (oral vancomycin), in phase 3 trials for Clostridium difficile-associated diarrhea (CDAD), the phase 3 bevenopran for opioid-induced constipation, and CB-618, a beta-lactamase inhibitor in early safety studies.

The company expects phase 3 Surotomycin CDAD top-line data in mid-2015 (NCT01598311). Although Surotomycin showed similar cure rates relative to vancomycin in phase 2, its differentiation is based on statistically significant (p<0.035) reductions in recurrence rates: at day 40, patients in the vancomycin arm had a recurrence rate of 36%, versus 17% in the Surotomycin arm.

Bevenopran is currently undergoing long-term safety trials: enrollment of 1,400 in a long-term phase 3 trial (NCT01696643) was completed in Q1 2014. Patients are randomized to either bevenopran at a dose of 0.25 mg BID or placebo for 52 weeks. Cubist has said it plans to initiate phase 3 efficacy trials after receiving safety data from the current trial and further discussions with the FDA. Based on existing data, Bbvenopran has the potential to offer comparable efficacy to other OIC therapies in development, but with a significantly reduced side effect profile.

Cubists’ deep pipleine is compelling, and as Sivextro and ceftolozane/tazobactam move closer to securing regulatory approval investor focus will turn to the remainder of the company’s pipeline.

Takeover Target?

While our thesis regarding Cubist has been based on the company’s position as a standalone company, reports surfaced in late April that Cubist has become a target for Shire (SHPG) in a complex web of takeover defenses in which Shire is eying Cubist as a defense against an Allergan (AGN) takeover (Allergan is reportedly eying Shire in order to remain independent amidst Valeant’s (VRX) offer to acquire the company). Cubist would be a complementary fit for Shire, which could combine operations with the antibiotic assets acquired from ViroPharma, as well as place future profits under a favorable tax jurisdiction. Cubist’s present size (an enterprise value of less than $5.5 billion) means that the company could be digestible for any number of pharmaceutical companies.

Regardless, rarely do these speculation-fueled reports pan out, and we suggest leaving the acquisition potential out of the investment decision entirely.

Cubist is well positioned for a return to profit growth as the company expands its business with two new products. A favorable landscape for antibiotics developers and the possibility of further regulatory assistance certainly helps. Cubist continues to strengthen its position as the leading pure-play and publicly traded antibiotics company, a title we believe will serve shareholders well over the long-run.

One or more of PropThink’s contributors are long CBST or CEMP.